Private Equity Bought America's Essential Services

Mirrored from Hacker News — AI on Front Page for archival readability. Support the source by reading on the original site.

May 23, 2026 | Economy

When a fire truck fails to deploy in a burning building and four people die, the cause isn’t just mechanical failure. It’s a business model.

On the night of June 26, 2025, firefighters on Tower Ladder 14 raced to a Chicago apartment building where an arsonist had poured gasoline on both stairwells. When they arrived, the aerial ladder would not go up. The crew had to shut the rig off entirely and restart it. The delay lasted approximately one minute. Four people died that night — including a pregnant woman, her five-year-old son, and her sister, who threw her own child from a third-floor window before perishing herself.

Nobody told the surviving family about the ladder malfunction. They found out from journalists.

That malfunctioning truck is a thread. Pull it, and what unravels is one of the clearest illustrations of how private equity — the $9.4 trillion industry that quietly controls roughly 11,500 American companies and 11 million jobs — turns essential public infrastructure into profit extraction machines, often at lethal cost.

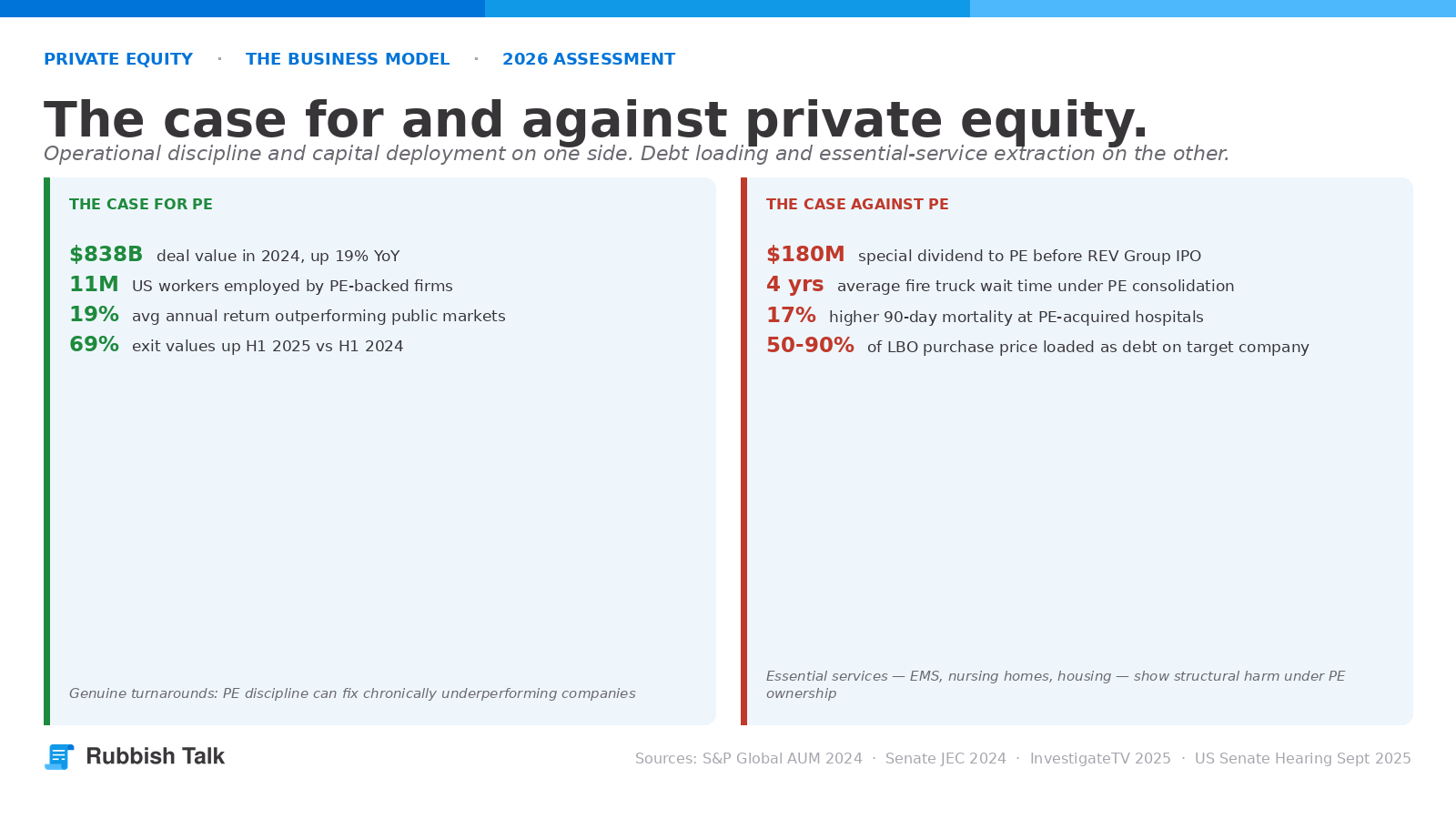

The Business Model: Brilliant for Investors, Brutal for Everyone Else

Private equity is not a mystery. The mechanics are straightforward, the incentives are transparent, and the outcomes are predictable once you understand how the machine works.

A private equity firm raises a fund — typically from pension funds, sovereign wealth funds, endowments, and wealthy individuals. It then acquires companies, usually through a leveraged buyout (LBO): a structure where 50 to 90 percent of the purchase price is financed by debt, and that debt is loaded onto the balance sheet of the acquired company, not the firm making the acquisition. The firm then charges the fund a management fee — historically 2 percent of assets annually — plus carried interest: a 20 percent cut of any profits, taxed at the long-term capital gains rate of 20 percent rather than the ordinary income rate of 37 percent. Critics have long called this a tax loophole. Congress has debated closing it for two decades and has not.

US private equity AUM reached $3.128 trillion in 2024 alone, according to S&P Global. Total private markets AUM globally sits at approximately $15 trillion.

The model works when applied to underperforming businesses that genuinely need restructuring. PE firms can bring operational discipline, growth capital, and strategic focus. That is the affirmative case, and it is real.

The problem emerges when the model is applied to essential services with inelastic demand — industries where the customer has no choice but to pay, where quality degradation is hard to measure until catastrophe strikes, and where the typical PE timeline of 3-to-7 years before exit creates incentives to strip value rather than build it.

The Senate Joint Economic Committee’s July 2024 report described this as a “buy, strip and flip” business model: PE firms load acquired companies with debt, cut costs aggressively, then resell at a profit — often at the direct expense of workers, communities, and the services those companies provide. Public companies acquired by PE are approximately ten times more likely to go bankrupt than a comparable control group subject to the same market forces, the report found.

The Fire Truck Racket: A Case Study in Manufactured Scarcity

The fire truck industry is the sharpest and most documented example of what PE consolidation does to essential services.

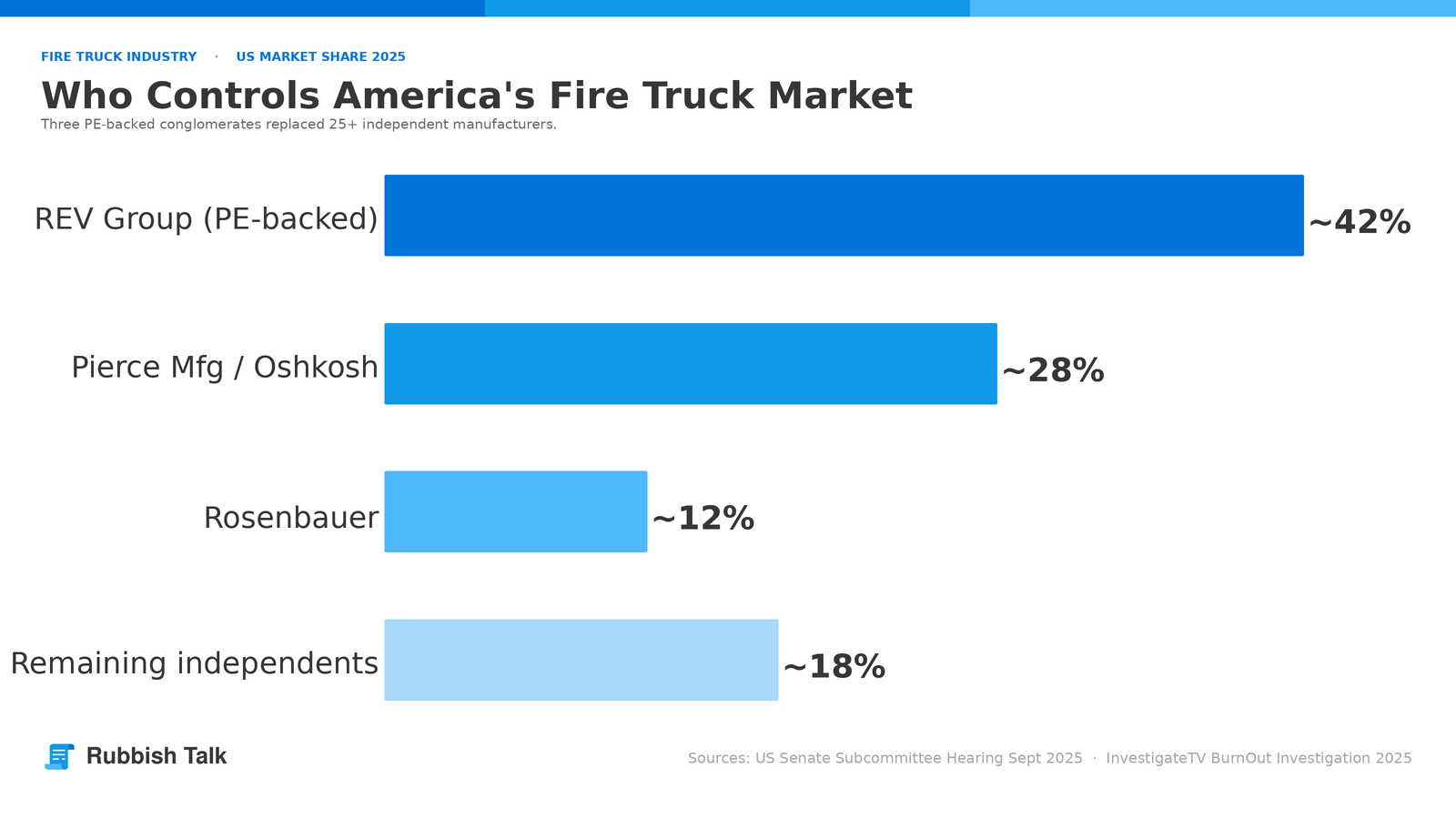

Two decades ago, more than two dozen independent manufacturers competed to build America’s fire apparatus. Today, three companies control approximately 80 percent of the market: REV Group, Pierce Manufacturing (owned by Oshkosh Corporation), and Rosenbauer. This concentration was not an accident of market forces. It was engineered.

REV Group is the centrepiece of the story. The company — owned by private equity firm American Industrial Partners — systematically acquired formerly independent manufacturers including E-One, Ferrara, KME, Ladder Tower, and Spartan. The old nameplates still exist as brand names. But behind them sits a single PE-backed conglomerate controlling a massive share of the supply chain for emergency vehicles that every American city depends on.

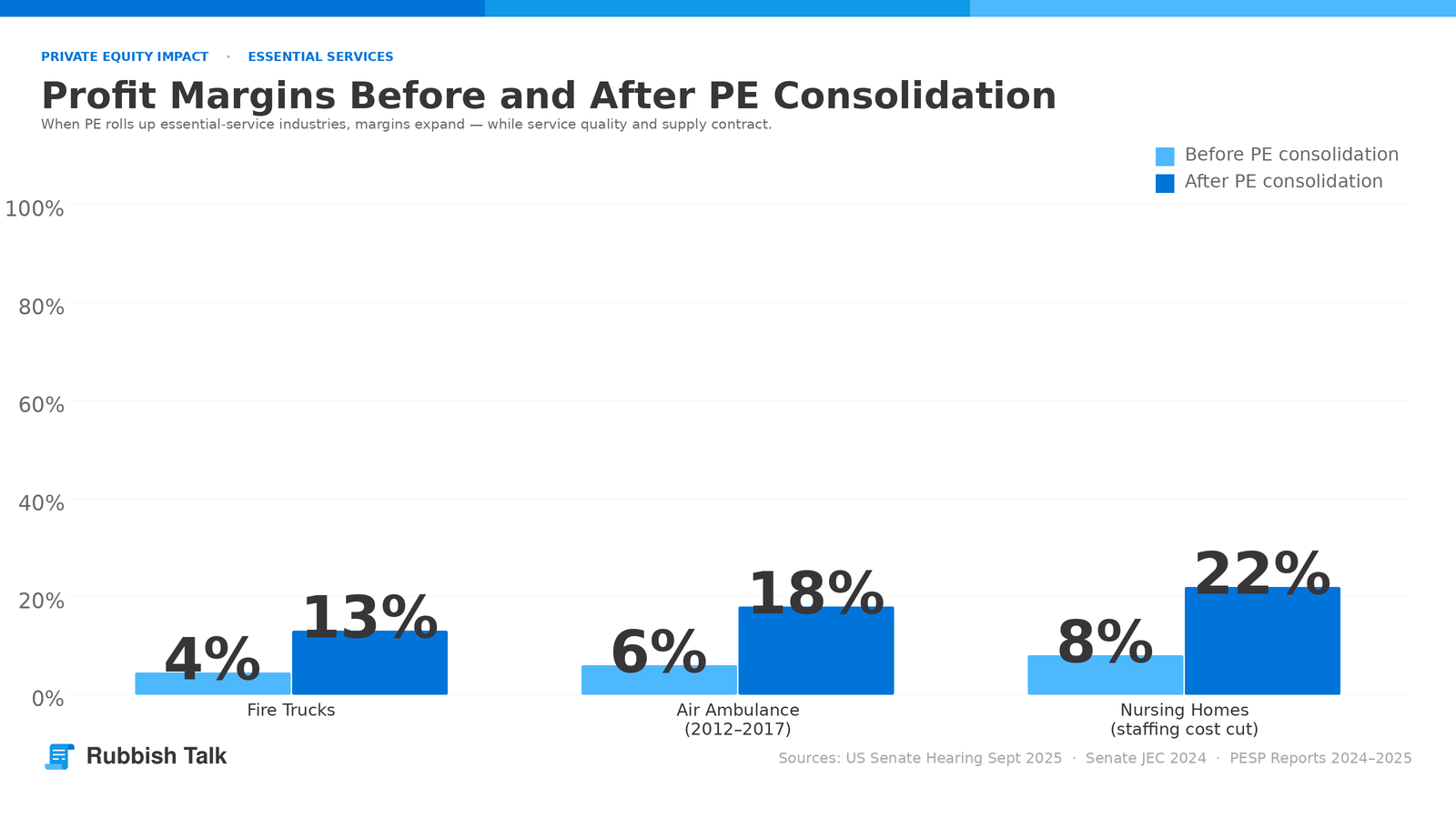

The result is a backlog that reads like a financial opportunity in earnings calls and a crisis in every fire station in the country. As of 2025, REV Group’s backlog stands at $4.5 billion. Wait times for a custom fire truck run to four years. Prices have doubled in a decade: a pumper truck now costs around $1 million; a ladder truck runs over $2 million. Profit margins in the industry have tripled — from the historic 4-to-5 percent range to over 13 percent.

“Our $4.5 billion backlog is attractive among industrial manufacturers, is largely backed by municipal tax receipts, and offers significant value accretion opportunity, providing a pathway for growth and margin expansion over the next several years.”

— Mark Skonieczny, CEO, REV Group, 2025 investor earnings call

Note what Skonieczny is telling investors: the backlog is not a problem to be solved. It is an asset. The customers — fire departments serving American cities — are locked in because they have no alternative. Their orders, backed by tax receipts, are guaranteed revenue. The company’s incentive is to maintain the backlog, not eliminate it.

The Senate heard this clearly. At a September 10, 2025 hearing, Senator Josh Hawley (R-MO) put it bluntly to the manufacturers:

“This didn’t just happen to you accidentally. This is a business decision, isn’t it? You keep these backlogs like this. […] Another word for this would be a heist. This sounds to me like private equity came in; bought up all of these small companies; combined them; shut down their production; rolled up a huge backlog; massive profits; stiffed these guys; and now you’re making out like bandits.”

— Sen. Josh Hawley, US Senate Subcommittee on Disaster Management, September 10, 2025

The production data supports Hawley’s characterisation. REV Group closed multiple production facilities in Pennsylvania and Virginia even as its backlog grew. The company simultaneously spent $530 million on stock buybacks and dividend payments, including a $180 million special dividend paid directly to private equity owners just before the company went public. The CEO earns $6 million annually.

The competitive market is gone. The Fire Apparatus Manufacturers Association — the industry trade group — holds annual meetings where members share “economic data, fire market trends, and apparatus sales and order statistics.” Antitrust attorney Basel Musharbash testified to Congress that the conglomerates “appear to have transformed a once vibrant industry into a racket.” Four cities — Los Angeles County, Green Bay, Allentown, and others — have filed federal antitrust lawsuits. The Texas Attorney General opened a price-fixing investigation. The defendants deny all wrongdoing.

Meanwhile, Ed Kelly, president of the International Association of Fire Fighters, told the Senate: “Sometimes we have firefighters responding in pickup trucks, like a painting crew with ground ladders on it.”

This Is a Pattern, Not an Anomaly

The fire truck industry is the most publicly documented case, but the underlying playbook — acquire, consolidate, reduce supply, extract margin — appears across essential sectors with alarming consistency.

Ambulances

Private equity’s grip on emergency medical services follows the same arc. KKR controls significant ambulance market share through Envision Healthcare and Global Medical Response (parent of Rural/Metro). As PE’s market share in air ambulance grew, the median charge for a transport increased over 60 percent between 2012 and 2017, according to research cited in Senate testimony. The predictable endpoint: Envision Healthcare filed for Chapter 11 bankruptcy in 2023 under the weight of debt it was saddled with after its PE acquisition — leaving contracts cancelled, response times degraded, and in at least one documented case, a delayed ambulance arrival that may have contributed to a death.

Nursing Homes

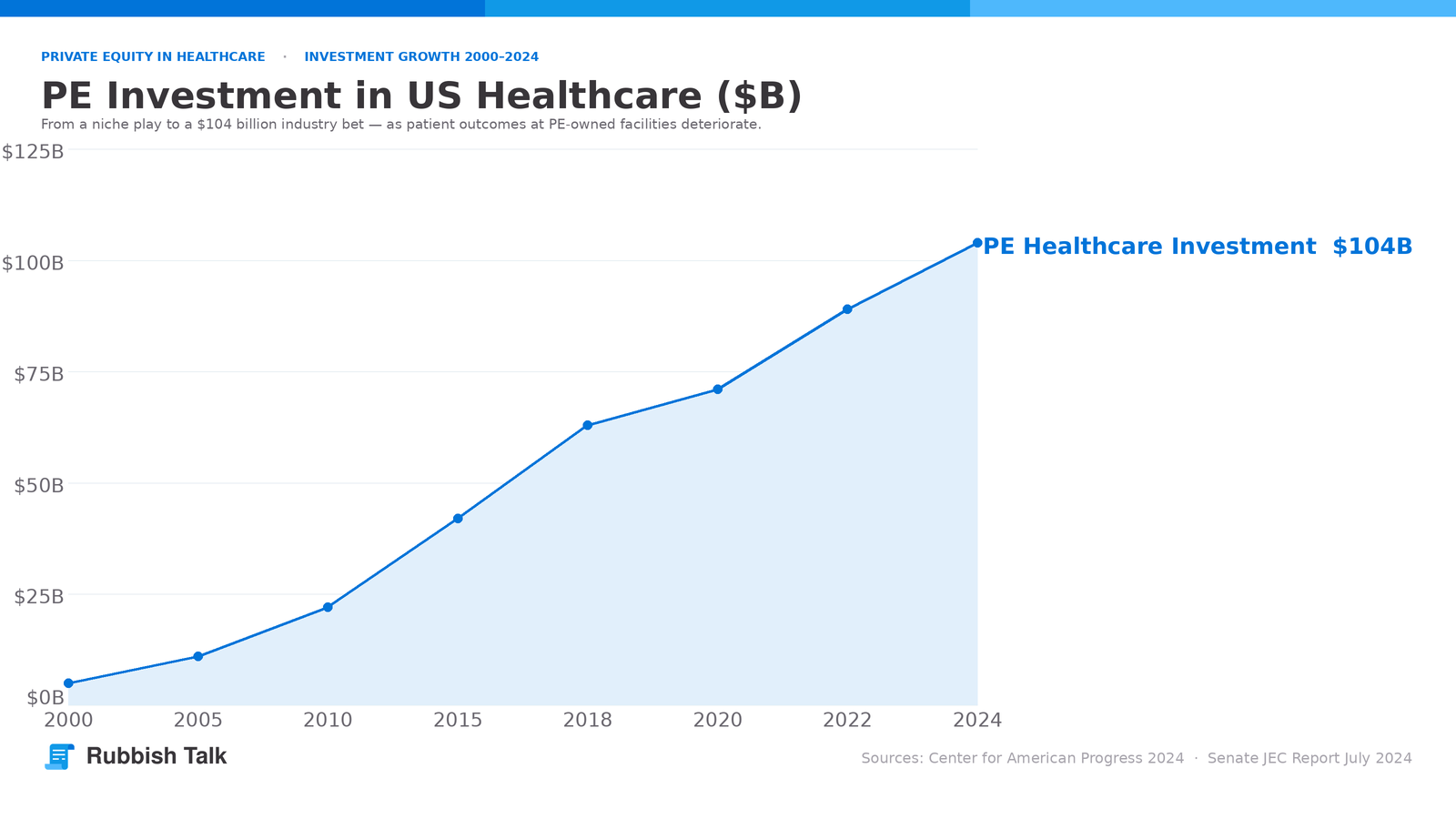

PE investment in nursing homes grew from $5 billion in 2000 to $104 billion in 2024. More than 1,500 facilities now operate under PE control. The documented outcomes are not ambiguous: PE-owned nursing homes show more care deficiencies, significantly reduced staffing hours, higher hospitalisation rates, and increased mortality. People undergoing surgery at PE-acquired hospitals faced a 17 percent higher probability of dying within 90 days than patients at non-acquired centres, according to peer-reviewed research. At least two PE-owned nursing home chains filed for bankruptcy in 2024 alone — LaVie Care Centers (backed by Formation Capital) and Goldner Capital Management — leaving residents displaced and staff unpaid.

Housing

Institutional investors — many PE-backed — own more than 500,000 single-family rental homes and are projected to control 40 percent of the US single-family rental market by 2030. The DOJ opened a criminal investigation in 2024 into RealPage, a property-management software firm used by major landlords, over allegations that its algorithmic pricing system enabled coordinated rent increases across competing landlords — effectively automating what antitrust law would otherwise prohibit. The Senate passed a bipartisan housing bill in March 2026 targeting large investors, though its scope remains limited.

Local Newspapers

Alden Global Capital — a hedge fund with tactics indistinguishable from PE — systematically acquired local newspapers and gutted them, cutting newsrooms faster than any other owner in the country. The 2019 Gannett-GateHouse merger, backed by New Media Investment Group (a hedge fund), put one in five US daily newspapers under financial-engineer control. Academic research found that when a PE firm acquires a newspaper, the newsroom shrinks by an average of nine reporters and editors — around 14 percent of staff — not because the papers aren’t profitable, but because the model demands margin extraction. The effect is the destruction of local democratic accountability infrastructure.

The Structural Problem Nobody Is Naming

The mainstream coverage of PE tends to focus on individual cases: a hospital that went bankrupt, a nursing home with code violations, a city that can’t get a fire truck for four years. The stories are compelling. What they often miss is the systemic architecture that makes these outcomes not bugs but features.

PE’s structural incentive is to maximise returns over a 3-to-7 year investment horizon. When applied to genuinely competitive industries with multiple players, this can drive efficiency. When applied to essential services — particularly after roll-up acquisitions that eliminate competition — it creates something more troubling: a model that profits from degradation of the very services the public cannot opt out of.

The debt loading mechanism is key and underreported. When a PE firm acquires a nursing home chain or an ambulance company via LBO, the debt doesn’t sit on the PE firm’s balance sheet. It sits on the acquired company’s balance sheet. The firm has already extracted its management fees. If the company eventually files for bankruptcy, the PE firm has typically already received dividends and fees that exceed its equity contribution. The losses fall on creditors, workers, pension funds, and — in the case of essential services — the communities that depended on those services.

REV Group’s $180 million special dividend to PE owners before IPO is a textbook example. The money was extracted before the market ever had a chance to price in the risk. The fire departments who need the trucks have no equivalent exit option.

What Comes Next

Four cities have now sued the major fire truck manufacturers. The IAFF has formally asked the FTC to investigate antitrust violations. The Senate held a bipartisan hearing — notable for its rarity — in which senators from both parties used words like “heist” and “racket” without the manufacturers offering a credible rebuttal.

The broader PE reform debate has gained ground. The Stop Wall Street Looting Act, introduced in Congress, would make PE firms liable for the debts of their portfolio companies, close the carried interest tax loophole, restrict dividend recapitalisation (the practice of loading debt to pay PE owners before exit), and give workers a priority claim in bankruptcy. It has not passed.

The harder question — one that the antitrust suits and Senate hearings won’t fully resolve — is whether essential infrastructure should be subject to the same financial-engineering logic as any other investable asset class. The market answer is: whatever generates return is fair game. The public service answer is: some industries exist to serve communities, and the cost of making them pure profit vehicles is paid in delayed ambulances, unmaintained fire trucks, and bodies in burned apartments.

The fire in Chicago is not a metaphor. It is a consequence. And it will keep happening until the structural incentives that produced it are addressed — not case by case, but at the level of the model itself.

Sources:

Discussion (0)

Sign in to join the discussion. Free account, 30 seconds — email code or GitHub.

Sign in →No comments yet. Sign in and be the first to say something.